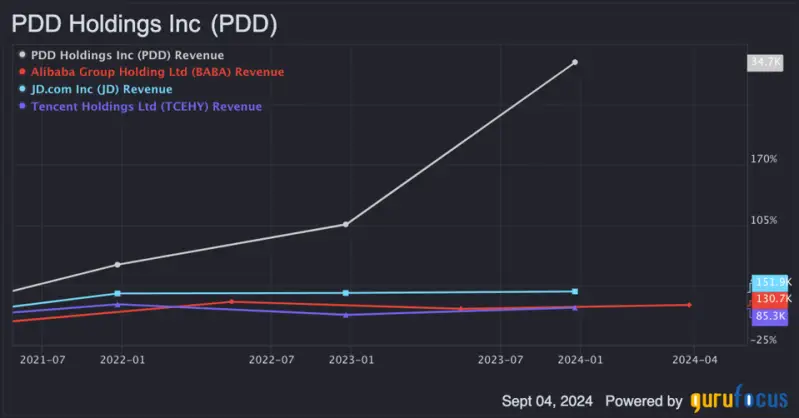

$PDD IS A GROWTH GIANT!

When the company IPO-ed in 2018, $BABA (37%) and $JD (18%) had dominance in e-commerce in China, but it took $PDD only 5 years to beat $JD and come in second place with 19.6% of the e-commerce market and to put pressure on $BABA while matching the Ablibaba's Taobao. By the 2022 $PDD has already matched number of active users Tmall and Taobao (two major e-commerce platforms operated by Alibaba) had together, and it also surpassed $JD in the same segment already in 2019. While $PDD's revenue was growing at 63%/year in 2023, $BABA was growing at 8%/year and $JD grew at 4.7%/year.

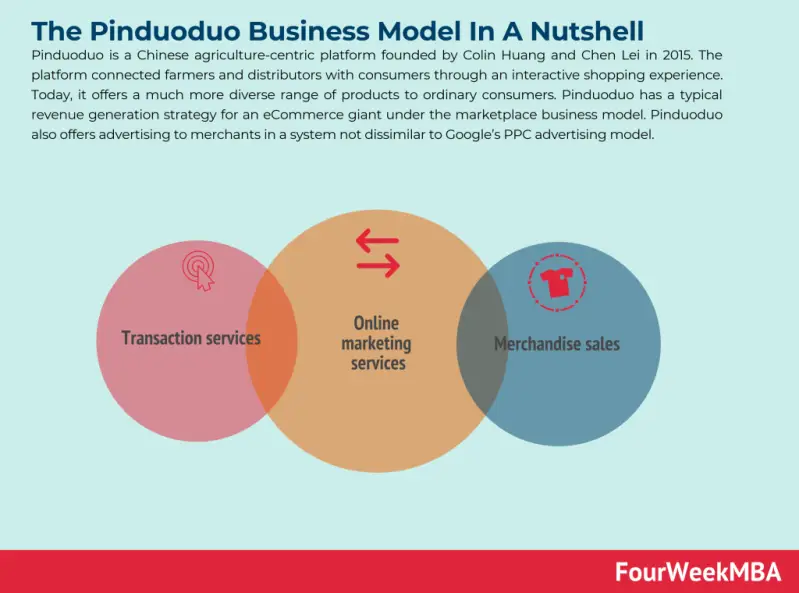

$PDD'S BUSINESS MODEL

$PDD's business model was built to get as many possible orders at the highest possible frequency, and the annual frequency of orders per buyer grew from 17.5x in 2017 to 115x in 2023, which means people were buying almost every third day. (365 days/115 annual orders per buyer = avg order of 3.17 days). Competitors $BABA and $JD had annual frequency of orders per buyer of 52x and 14x in 2023. The difference is range of selection is that $PDD has diversified product categories which have high frequency of buys, while other e-commerces have only one or two product categories. This gave $PDD edge to grow annual spend per active buyer from $82 in FY17 to $618 in FY23, while $BABA didnt move much from $1,185 in FY17 to $1,115 in FY23, and $JD grew slowly from $443 in FY17 to $584 in FY23.

$PDD GETTING ACCEPTED AS MAJOR PLAYER

After years of being profitable, $PDD is getting seen at the sustainable business from the anaylist and investors. After becoming a profitable company in 2021, net profit margin grew from 8.27% in 2021 to 28.55% in 2024. With the launch of Temu in 2022, $PDD's gross profit margins decreased by -10%, and $PDD increased its cost efficiency (+7%) by customer acquisition cost, fulfillment cost, and growing gross profit margins through increasing average order value. $PDD did same thing with Temu they did with they DDG (grocery delivery business), first they subsidized big in the first stage, then they cut costs and finally they became profitable.

$PDD BEATING THE FALSE NARRATIVES

Previously, many believed $PDD's business model was unsustainable, assuming its low prices relied solely on significant platform subsidies, and that competitors $BABA and $JD could easily hinder $PDD's growth through price competition. But.. $PDD has achieved a high EBIT margin by leveraging unique business model features that create a cost-efficient structure, boost rapidly growing annual spending per buyer, and drive increased advertising revenue. $PDD now directs its Sales and Marketing expenses toward boosting Gross Merchandise Volume growth and increasing take-rates, achieving improved marketing efficiency. In contrast, $BABA has experienced declining marketing efficiency, while $JD has shown no significant change.

$PDD'S ADVANTAGE IN MARKETING SERVICES

While $BABA and $JD are charging fees to merchants and taking percentage of the sale, $PDD is making money from marketing serivces they provide to OEMs. OEMs are companies that produce parts and products that are then marketed and sold by another company. This model lowers the cost for suppliers, and OEMs use the platform's marketing tools. Instead of relying solely on SEO keyword bidding, PDD uses diverse promotional tools and multiple traffic sources to engage customers in various ways. This allows merchants to customize their marketing spending according to product sales, audience, etc, and by doing that, merchants increase their return on investment.

IMPORTANCE OF $PDD'S TEMU

Temu, launched in July 2022, rapidly surpassed expectations by overtaking Shein's daily sales by October 2023, pressuring Shein to pursue an early IPO. Temu's growth primarily comes at the expense of AliExpress, Shein, and discount retailers, with its model relying on low supplier prices, heavy subsidies, and aggressive advertising. While $AMZN remains insulated, catering to middle-income families, Temu appeals to merchants with lower fees (30-50% cheaper listings than Amazon), despite Amazon's high costs (28% fulfillment, 12% commission, 12% advertising). Temu’s Roadmap and Achievements: 2022: Aimed for 3M sellers and 2M customers by December, achieving 13M daily active users by March 2023. 2023-2024: Focus on breaking even through product optimization, raising GMV targets from $3B to $10B for 2023. 2025: Targets full profitability across markets. Temu doubled its average order value (AOV) from $20 to $40 by shifting from clothing to standardized household and personal care products, with 30% of GMV from electronics, 25% from home decor, and 20% from apparel. This diversification helped Temu brand itself as a value-for-money platform, unlike Shein, where apparel still dominates (75% of GMV).